All Categories

Featured

Table of Contents

nfinite banking is a financial strategy that empowers you to take control of your finances using the cash value of a whole life insurance policy. By becoming your own banker, you can leverage the cash value to fund large expenses, invest in business opportunities, or handle emergencies—all while your money continues to grow tax-free. For business owners, infinite banking is an invaluable tool for maintaining financial independence and flexibility.

Whole life insurance policies designed for infinite banking offer stability and predictability, ensuring steady cash value growth over time. best term life insurance for 2025 agents. Policies with living benefits further enhance their appeal, offering access to funds for critical illnesses or other urgent needs. Whether you’re looking to finance major purchases, grow your business, or achieve financial independence, infinite banking adapts to your goals while providing long-term security

This concept is especially beneficial for individuals and families seeking flexible financial solutions or business owners aiming to optimize their cash flow. Learn more about how infinite banking can transform your financial future. Schedule a free consultation today and take the first step toward achieving complete financial control.

That usually makes them a much more budget friendly option for life insurance protection. Several people get life insurance policy coverage to assist monetarily safeguard their enjoyed ones in situation of their unexpected fatality.

Or you might have the choice to convert your existing term protection into an irreversible plan that lasts the rest of your life. Numerous life insurance policies have potential benefits and drawbacks, so it's important to understand each before you determine to buy a plan.

As long as you pay the premium, your beneficiaries will certainly receive the death advantage if you die while covered. That claimed, it is necessary to keep in mind that the majority of plans are contestable for two years which implies coverage might be retracted on death, must a misrepresentation be located in the application. Policies that are not contestable typically have a rated death advantage.

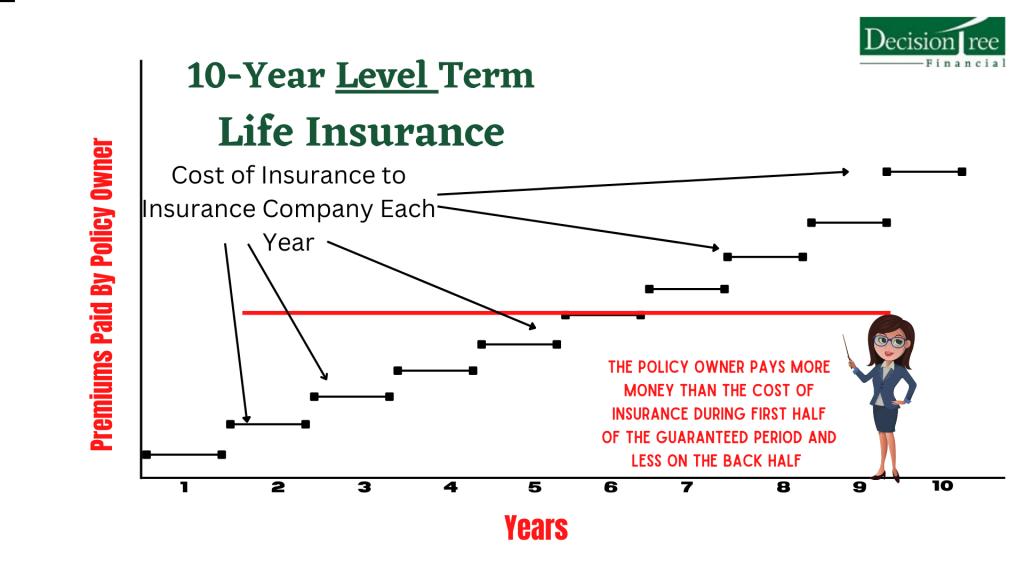

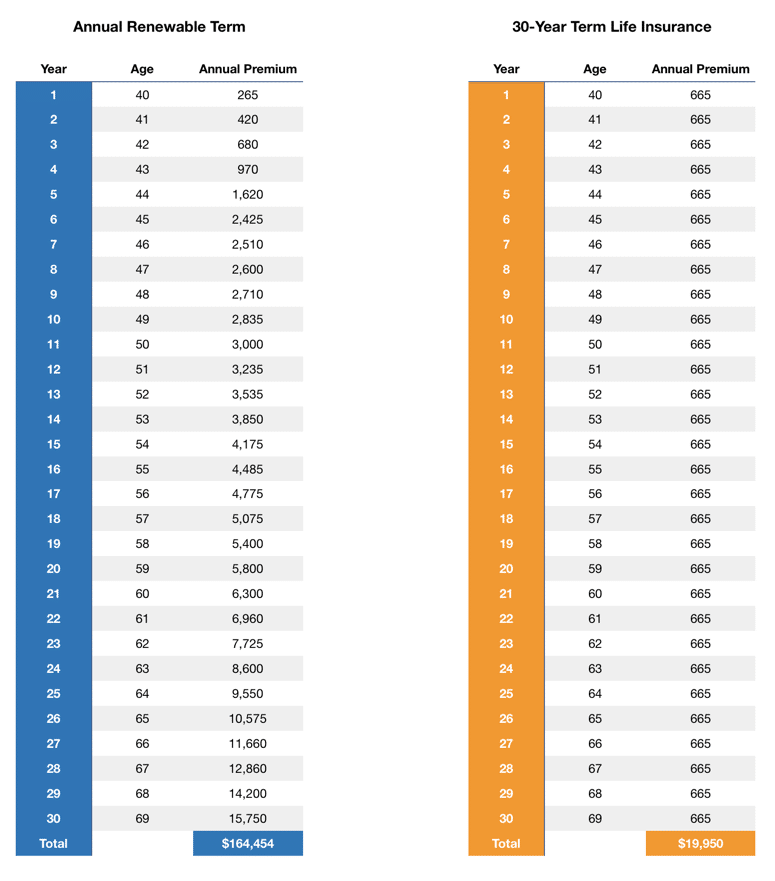

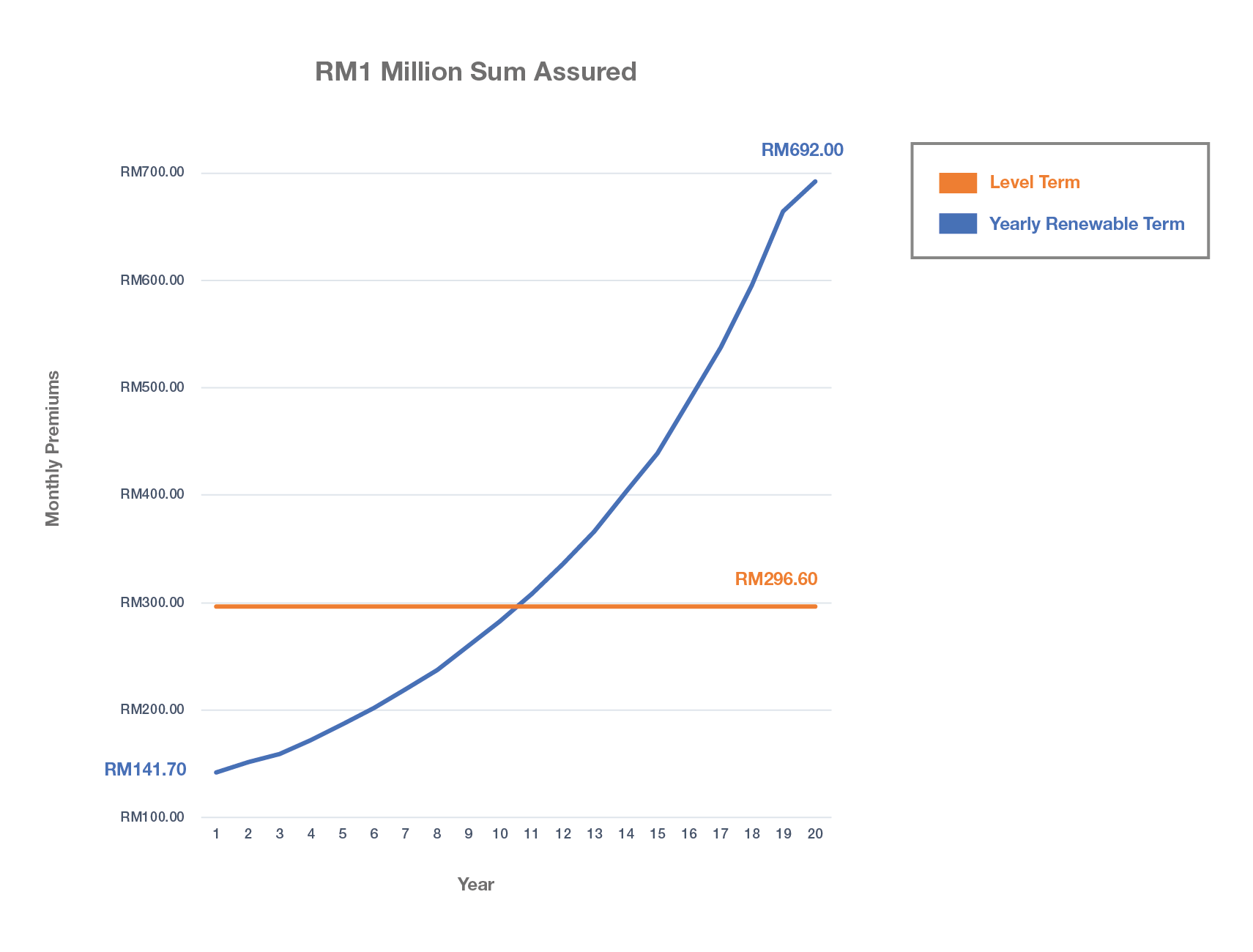

Costs are typically reduced than whole life plans. With a degree term policy, you can choose your protection quantity and the plan length. You're not locked into a contract for the remainder of your life. Throughout your policy, you never need to stress over the costs or survivor benefit quantities altering.

And you can't squander your policy during its term, so you won't get any financial benefit from your past protection. Similar to other types of life insurance policy, the expense of a level term plan relies on your age, protection requirements, employment, way of life and health and wellness. Usually, you'll locate more inexpensive insurance coverage if you're younger, healthier and much less dangerous to guarantee.

Premium Level Term Life Insurance Meaning

Given that degree term costs stay the same for the duration of insurance coverage, you'll recognize exactly just how much you'll pay each time. That can be a huge aid when budgeting your costs. Degree term coverage likewise has some adaptability, enabling you to personalize your plan with additional attributes. These commonly come in the form of bikers.

You might have to fulfill particular problems and qualifications for your insurance firm to establish this motorcyclist. There also can be an age or time limit on the protection.

The fatality benefit is usually smaller sized, and coverage usually lasts up until your child transforms 18 or 25. This motorcyclist might be an extra cost-effective means to assist guarantee your youngsters are covered as riders can typically cover multiple dependents at when. Once your youngster ages out of this insurance coverage, it may be feasible to convert the biker into a brand-new policy.

When contrasting term versus long-term life insurance policy. level term life insurance definition, it is necessary to keep in mind there are a few various types. The most typical type of permanent life insurance policy is entire life insurance policy, yet it has some essential differences compared to degree term protection. Below's a basic overview of what to think about when comparing term vs.

Whole life insurance policy lasts forever, while term coverage lasts for a certain duration. The premiums for term life insurance coverage are usually less than whole life insurance coverage. With both, the costs stay the very same for the duration of the policy. Whole life insurance coverage has a cash value component, where a portion of the costs might expand tax-deferred for future needs.

One of the major functions of level term coverage is that your costs and your death benefit do not transform. You might have coverage that begins with a fatality benefit of $10,000, which could cover a home loan, and after that each year, the fatality advantage will certainly lower by a collection quantity or percentage.

Due to this, it's frequently a much more budget friendly kind of degree term protection. You might have life insurance policy through your company, however it might not be enough life insurance for your demands. The very first step when purchasing a policy is figuring out just how much life insurance policy you need. Think about variables such as: Age Family members dimension and ages Work status Revenue Debt Lifestyle Expected last costs A life insurance policy calculator can assist identify just how much you require to begin.

After choosing on a policy, finish the application. If you're accepted, authorize the documentation and pay your very first premium.

Tailored Level Term Life Insurance

You might want to update your beneficiary details if you have actually had any significant life adjustments, such as a marital relationship, birth or divorce. Life insurance policy can often feel challenging.

No, level term life insurance coverage does not have cash worth. Some life insurance policy policies have an investment attribute that permits you to develop cash money value over time. A part of your premium repayments is reserved and can make interest over time, which expands tax-deferred throughout the life of your coverage.

However, these policies are often significantly much more costly than term coverage. If you reach completion of your policy and are still to life, the protection ends. You have some choices if you still desire some life insurance protection. You can: If you're 65 and your protection has gone out, for instance, you may want to get a brand-new 10-year degree term life insurance policy policy.

Cost-Effective Joint Term Life Insurance

You might have the ability to transform your term insurance coverage right into an entire life plan that will last for the rest of your life. Many sorts of degree term plans are convertible. That suggests, at the end of your coverage, you can convert some or all of your plan to whole life insurance coverage.

Degree term life insurance coverage is a policy that lasts a collection term usually in between 10 and three decades and includes a degree survivor benefit and level premiums that stay the same for the entire time the policy holds. This indicates you'll recognize precisely how much your payments are and when you'll need to make them, permitting you to budget appropriately.

Level term can be a fantastic option if you're wanting to acquire life insurance protection for the very first time. According to LIMRA's 2023 Insurance Barometer Research, 30% of all grownups in the U.S. requirement life insurance coverage and do not have any kind of plan. Level term life is foreseeable and inexpensive, which makes it one of the most prominent kinds of life insurance policy.

{kind=link}

Latest Posts

Types Of Final Expense Insurance

Final Expense Insurance Pa

Final Expense Whole Life Insurance Reviews